Australia is facing a looming fiscal crisis, as the gap between government spending and revenue widens and the population ages. There is also a tax imbalance.

The federal budget is in a “hell of a mess,” according to former Treasury secretary Ken Henry, who says the government is not collecting enough tax to fund the basic services Australians expect.

The problem is not new. For decades, experts have warned that Australia’s tax system is unsustainable and unfair, and that reforms are needed to ensure future generations are not burdened with higher taxes and lower living standards.

Ken Henry, former Treasury Secretary. NewsBlaze Cartoon.

Successive governments have failed to tackle the issue, preferring to avoid unpopular changes and rely on temporary fixes such as debt, asset sales and spending cuts.

Meanwhile, the challenges are mounting. The COVID-19 pandemic has exposed the fragility of Australia’s health and aged care systems, which are already struggling to cope with rising demand and costs.

The National Disability Insurance Scheme (NDIS), which provides support for people with disabilities, is projected to cost more than $30 billion a year by 2023-24.

Defence spending is set to increase by $270 billion over the next decade, as Australia faces a more uncertain and complex strategic environment.

And climate change poses a serious threat to Australia’s economy and environment, requiring urgent action and investment.

All these areas require adequate and stable funding, but the government’s revenue base is shrinking and eroding. The big question is why this has not been addressed already. Did they not see this coming?

Are governments and their advisors incompetent? It appears they know what they are doing. They already tried to cancel cash but their plan failed.

Huge Tax Imbalance

One of the main causes of Australia’s fiscal woes is the high degree of vertical fiscal imbalance (VFI), which means that the federal government collects most of the tax revenue, while the states and territories are responsible for most of the service delivery.

With just more than half of the service delivery responsibilities, the Commonwealth controls over 80 percent of all tax revenue – well in excess of its requirements.

This creates a mismatch between revenue and expenditure, and reduces the accountability and efficiency of both levels of government.

The states and territories depend on grants from the federal government to fund their services, such as health, education and transport. But these grants are often conditional, unpredictable and inadequate, leaving the states and territories with little fiscal autonomy or flexibility.

The federal government also transfers some of its revenue-raising powers to the states and territories, such as payroll tax and stamp duty. But these taxes are inefficient, distorting and inequitable, creating barriers to employment, investment and mobility.

The result is a complex and fragmented tax system that fails to meet the needs and expectations of Australians.

Shrinking Revenue Base

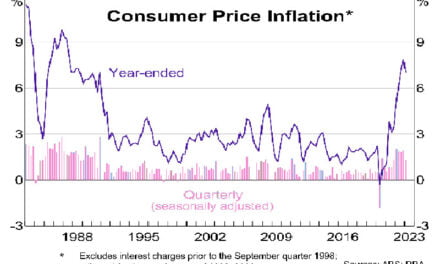

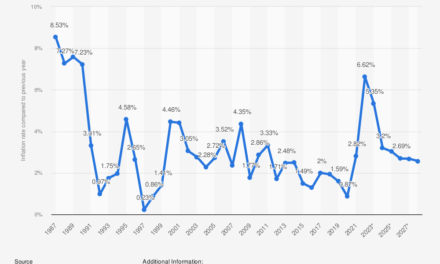

Another problem with Australia’s tax system is that it relies too heavily on income tax, which accounts for about half of all federal revenue. [ABC]

Income tax is progressive, meaning that people pay more as they earn more. This helps to reduce inequality and redistribute income to those who need it most.

But income tax also has its drawbacks. It discourages work, saving and investment, and it is vulnerable to economic shocks and demographic changes.

As Australia’s population ages, there will be fewer working-age people to pay income tax, while more people will rely on government benefits and services.

The Intergenerational Report (IGR), which projects the economic and fiscal outlook for Australia over the next 40 years, warns that this will put pressure on the budget balance and reduce economic growth.

The IGR estimates that by 2060-61, there will be only 2.7 working-age people for every person aged 65 and over, compared with 4.0 in 2020-21.

This means that there will be less income tax revenue per person to fund government spending per person.

The IGR also forecasts that income tax revenue will decline as a share of gross domestic product (GDP), from 11.6 percent in 2020-21 to 10.9 percent in 2060-61.

This reflects the fact that income tax brackets are not indexed to inflation or wage growth, meaning that people pay more tax as their incomes rise over time. This is known as bracket creep, which erodes people’s purchasing power and reduces their incentives to work.

The government has tried to address this issue by providing income tax cuts in recent budgets, but these cuts are not enough to offset the long-term effects of bracket creep.

Moreover, income tax cuts reduce the government’s revenue base without addressing the underlying structural problems of the tax system.

An Eroding Revenue Base

Another problem with Australia’s tax system is that it relies too little on consumption tax, which accounts for about a quarter of all federal revenue.

Consumption tax is regressive, meaning that people pay the same amount regardless of their income. This can be unfair and hurt low-income earners more than high-income earners.

But consumption tax also has its advantages. It encourages saving and investment, and it is more stable and resilient to economic shocks and demographic changes.

Unlike income tax, consumption tax does not depend on how much people earn, but on how much they spend. This means that it can capture revenue from a wider range of sources, such as tourists, foreign investors and the digital economy.

Consumption tax can also be used to influence people’s behaviour and choices, such as discouraging smoking, drinking and pollution.

The main form of consumption tax in Australia is the goods and services tax (GST), which is a 10 percent tax on most goods and services sold in Australia.

The GST was introduced in 2000 as part of a major tax reform package, which also included income tax cuts, compensation for low-income earners and changes to state taxes.

The GST replaced a number of inefficient and complex indirect taxes, such as wholesale sales tax, financial institutions duty and stamp duty on marketable securities.

The GST is collected by the federal government, but it is distributed to the states and territories according to a formula that aims to ensure horizontal fiscal equalisation (HFE), which means that each state and territory has the same fiscal capacity to provide services to its residents.

The GST was designed to be a broad-based and efficient tax that would grow in line with the economy and provide a reliable source of revenue for the states and territories.

But over time, the GST has become narrower and less effective, as more goods and services have been exempted or reduced from the tax base.

These include fresh food, education, health, childcare, water and sewerage services, financial services and residential rent.

These exemptions reduce the efficiency and equity of the GST, as they create distortions and inequities in the market and favour some sectors over others.

They also reduce the revenue potential of the GST, as they exclude some of the fastest-growing areas of consumption from the tax base.

According to the Productivity Commission, the GST covers only about 55 percent of total consumption in Australia, compared with an average of 65 percent for other OECD countries.

This means that Australia has one of the lowest GST revenue ratios in the world, at 3.6 percent of GDP in 2019-20.

The Productivity Commission estimates that if Australia applied the GST to all consumption at a rate of 10 percent, it would raise an additional $25 billion a year.

Alternatively, if Australia increased the GST rate to 15 percent while maintaining the current exemptions, it would raise an additional $35 billion a year.

Either option would significantly boost the government’s revenue base and reduce its reliance on income tax.

But both options would also have significant distributional impacts, as they would increase the cost of living for consumers and affect different income groups differently.

To address these impacts, the government would need to provide compensation for low-income earners and adjust other taxes and transfers accordingly.

This would require political courage and public support, which have been lacking in recent years.

Australian government tax revenue less than they spend. Image by 3D Animation Production Company from Pixabay

A Need for Reform

Australia’s tax system is in urgent need of reform, as it fails to meet the principles of a good tax system: efficiency, equity, simplicity and sustainability.

The current system is inefficient, as it distorts economic decisions and reduces productivity and growth.

It is inequitable, as it imposes different tax burdens on different income groups and sectors.

It is complex, as it involves multiple taxes, exemptions, deductions and concessions that create confusion and compliance costs.

And it is unsustainable, as it does not generate enough revenue to fund the government’s spending commitments and obligations.

Many experts and organisations have called for a comprehensive review and overhaul of Australia’s tax system, to make it more fit-for-purpose and future-proof.

Some Proposed Reforms

• Broadening the GST base and/or increasing the GST rate, while providing compensation for low-income earners and adjusting other taxes and transfers accordingly.

• Abolishing or reducing inefficient and distorting state taxes, such as payroll tax and stamp duty, and replacing them with more efficient and equitable taxes, such as land tax and road user charges.

• Simplifying and flattening the income tax system, by reducing the number of tax brackets and rates, eliminating or capping deductions and concessions, and indexing thresholds to inflation or wage growth.

• Introducing a more comprehensive capital gains tax (CGT), by removing or reducing exemptions for the family home, superannuation and small businesses, and aligning the CGT rate with the income tax rate.

• Reforming the corporate tax system, by lowering the corporate tax rate, broadening the corporate tax base, eliminating or reducing loopholes and incentives, and harmonising the tax treatment of domestic and foreign investors.

• Implementing a carbon tax or emissions trading scheme (ETS), by putting a price on carbon emissions and using the revenue to fund environmental initiatives and compensate affected households and businesses.

• Enhancing the progressivity and adequacy of the social security system, by increasing the JobSeeker rate, indexing payments to wage growth, simplifying eligibility criteria and taper rates, and strengthening mutual obligations.

Government spending more than it collects. Image by PIRO from Pixabay modified by NewsBlaze

Economic and Social Benefits

These reforms would have significant economic and social benefits for Australia, such as:

• Increasing economic efficiency, productivity and growth, by removing distortions and disincentives in the market and encouraging work, saving and investment.

• Improving fiscal sustainability and flexibility, by increasing revenue potential and reducing expenditure pressures for the government.

• Enhancing equity and fairness, by reducing inequality and redistribution income to those who need it most.

• Simplifying administration and compliance, by reducing complexity and confusion for taxpayers and authorities.

• Addressing environmental challenges, by reducing greenhouse gas emissions and promoting clean energy sources.

Political, Public Challenges

However, these reforms would also face significant political and public challenges, such as:

• Resisting vested interests and pressure groups, who would oppose any changes that would adversely affect their income or wealth.

• Overcoming public resistance and mistrust, who would be wary of any changes that would increase their tax burden or reduce their benefits.

• Balancing competing objectives and trade-offs, such as efficiency versus equity, simplicity versus flexibility, stability versus responsiveness.

• Coordinating with state and territory governments, who would have different preferences and priorities for tax reform.

• Communicating clearly and transparently with stakeholders, who would need to understand the rationale and implications of any changes.

These challenges explain why tax reform has been so difficult to achieve in Australia in recent years.

But they also highlight why the tax imbalance is so great and tax reform so necessary and urgent for Australia’s future.

{kind=link}